What is a SPAC?

A SPAC, or “blank-check company,” is a shell company formed with the intent of raising capital through an Initial Public Offering (“IPO”) for the sole purpose of acquiring an existing company. Upon completion of the transaction, the acquired company assumes the SPACs listing on the public exchange. SPACs are typically formed by a selected Management Team who claim a particular expertise in a certain business area and normally state an intention to pursue acquisition targets in those areas. Neither the IPO investors nor the SPAC managers know what company they will ultimately be investing in. One of the appeals of SPACs for potential target companies is the ability to become public companies through the process of an acquisition versus the traditional IPO process. One unique aspect of the SPAC process is that the SPAC must consummate the required acquisition within 24 months of formation, or the SPAC must be dissolved and the capital that was raised must be returned to its investors. This creates increased pressure on the SPAC managers to find a suitable target company to acquire within the required timeframe. This mandated timeline has been criticized as arguably creating an incentive for SPACs to chase transactions that may not be sound to avoid the alternative of not satisfying the 24-month requirement.

Why are we reading so much about SPACs now?

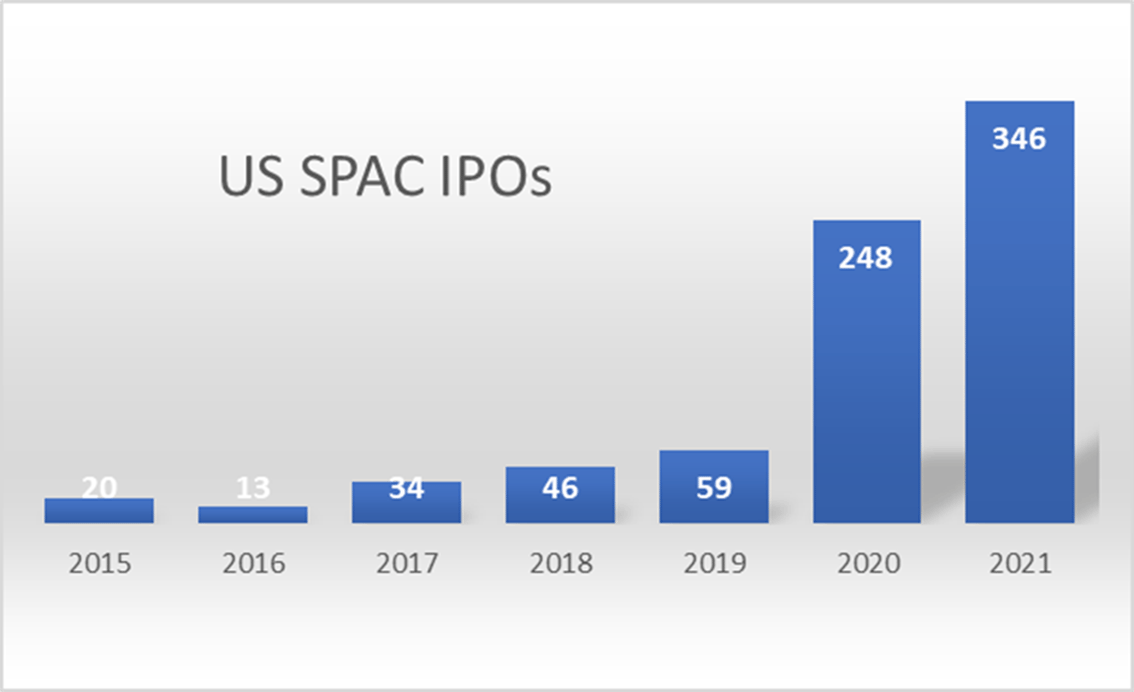

SPACs have existed for decades but, historically, were a seldom used method utilized by companies for going public. However, in 2019 we began to witness a seismic shift in the popularity of SPACs, which further accelerated in 2020. For example, in 2015 only 20 SPACs were formed. In contrast, nearly 250 SPACs were formed in 2020. This trend continued its acceleration into the first quarter of 2021, as demonstrated in the chart below.

*Source – www.spacresearch.com as of 6/22/21

The use of SPACs becoming much more frequent than traditional IPO’s combined with the high-profile nature, celebrity investors, and some significant failures have brought SPACs to the forefront of business headlines. This increased attention has led the Securities and Exchange Commission (“SEC”) to take a special interest in these investment vehicles. Most of the SEC’s focus has been trained on two specific areas. The first being that SPAC founders are incented with warrants. On April 12, 2021, the SEC issued a statement suggesting that they have concerns surrounding the accounting treatment of warrants issued by SPACs. The second concern is that the target companies can comment on business projections in a manner that is prohibited with a traditional IPO. It remains to be seen how much further the SEC pursues these concerns and whether they require changes or other oversight. In the short-term, this has had a meaningful effect on the number of SPAC formations in the second quarter or 2021, however, most expect their increased popularity to continue in the future.

Isn’t the Directors and Officers Liability exposure very similar to a traditional IPO?

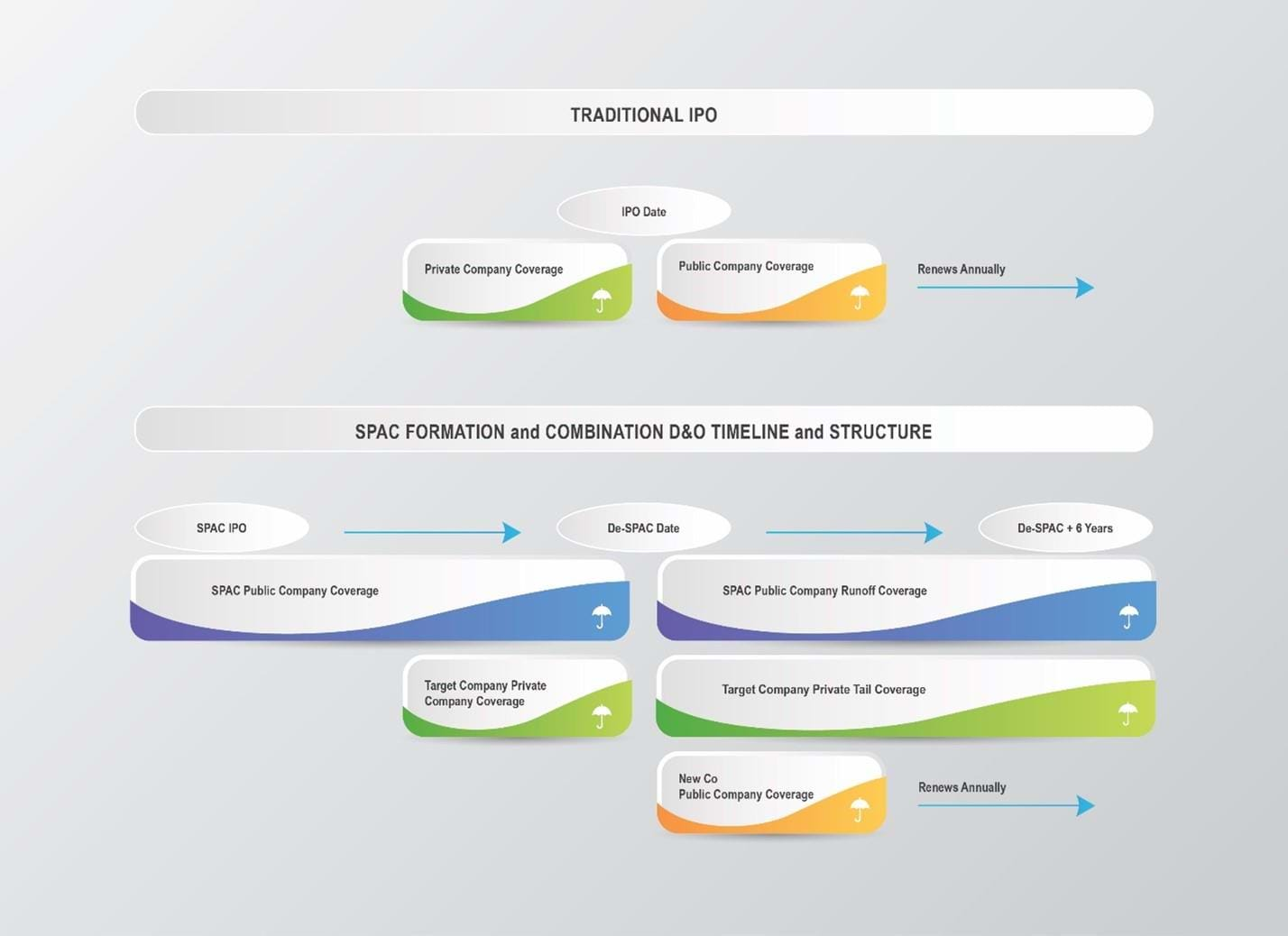

In a traditional IPO process, the insurance procurement process is often more straightforward than with the SPAC formation and combination process as many of the key players are consistent through the transition from private company to public company. For example, bankers, lawyers, and consultants work with the private company to prepare a roadshow, submit public filings, and, ultimately, list their stock for public offering. During this process, the Directors and Officer’s exposure transitions naturally from a private company D&O insurance program to a public company D&O insurance program. The interests of the private company’s Board of Directors and those of the new public companies’ Board of Directors are well aligned. The transition of the private company D&O program to the public D&O program is also typically managed by the same risk managers and management team together with one insurance broker.

Managing D&O insurance in the SPAC process is entirely different and creates the potential for additional pitfalls that need to be carefully navigated. For example, the process involves three different entities, three different Board of Directors and often involves two separate insurance brokers. The chart below illustrates how coverage is normally structured under these two very different processes.

Managing D&O coverage for SPACs requires close coordination between each of the three entities and the insurance brokers involved. Due to the nature of the process and some of the inherent pitfalls, the occurrence of claims after the de-SPAC are not uncommon and the potential for triggering one, two or all three of the insurance programs detailed above is possible. If these programs are not negotiated correctly gaps in coverage can exist and effective claims management can be problematic.

One of the challenges being seen in the current D&O insurance marketplace is with respect to the placement of coverage for a newly formed SPAC. Not unlike investors, underwriters are essentially being asked to evaluate a new public company with no access to financial statements, projections, balance sheets, operating company due diligence, etc. Rather, they are simply evaluating the quality of the management team assembled and their advisors. These facts, combined with the rapid acceleration of using SPACs and the very public failure of a handful of SPAC deals, have created a “hard” insurance market for SPACs, which has seen premiums and retentions rise over the last few years. These changes in the SPAC marketplace have brought SPAC D&O pricing more in-line with costs for D&O coverage in the traditional IPO marketplace. This has made it increasingly prudent to fully understand the negotiation and procurement process and even to consider whether other risk transfer tools might be better suited for some SPACs including captive insurance programs, etc. However, the fact that a SPACs lifespan is 24 months or less and that SPACs have limited capital resources beyond the funds raised in their initial offering can make alternative risk transfer tools difficult to make practical.

Best Practices for SPAC and Target Company Risk Managers?

- The Target Company managers should think and act like a public company long before they are public. This can be a cultural challenge for founders of private companies that are used to having much more flexibility in their actions and communications.

- Ensure your insurance broker understands the unique challenges the SPAC process presents.

- Require your insurance broker to coordinate coverage with the other entities broker(s) so that all three D&O policies are integrated and function as expected.

- Assume there will be a claim (likely after “de-SPAC”) and have a response process ready.

- Determine how the large, self-insured retention (typically $5M or higher) is going to be funded.

- Understand any indemnification arrangements and the in-force corporate bylaws.

- Strongly consider stand-alone Side A Coverage for individual directors and officers.